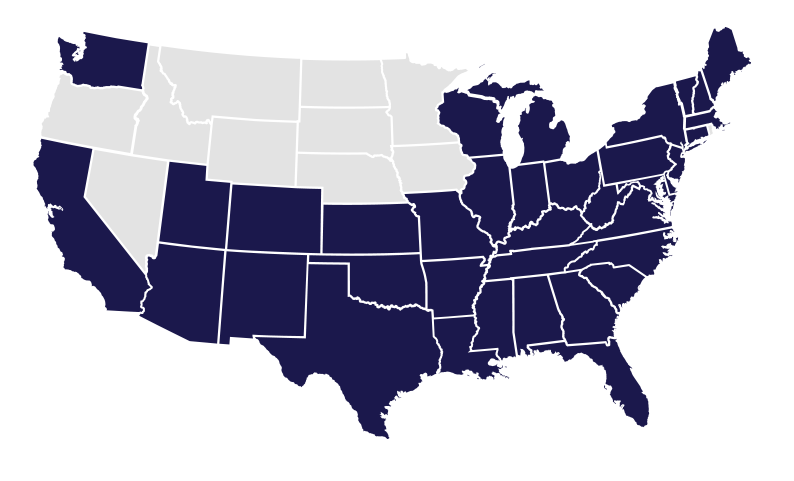

We provide easy access to fix-and-flip and rental loans for investment properties located in the following states — and we’re adding new markets all the time.

When you’ve found a good deal, you need to move fast. And you need a lender you can count on. We pride ourselves on our proven and vetted lenders who consistently deliver on time and under pressure because that’s when it matters most.

GET PRE-APPROVED

Your loan officer will work with you to understand your investment strategy, get you pre-approved, and provide a proof of funds letter should you need one.

Submit Your Deal

Once you have a deal, give your loan officer the documentation required to complete your loan and they’ll guide you through the underwriting and closing process.

Flip or Hold

Depending on your exit strategy, either rehab your investment property to resell within 12 months or buy and hold with a longer-term loan designed for landlords.

1

Submit a quick prescreen.

2

Receive prompt preapproval from lenders that match your loan needs.

3

Choose a lender and close your transaction.

"At Sherman Bridge, it’s possible to go to the moon and back in three days, like a Cosmonaut. My loan got approved on the same day and we did close in 3 business days! Their advice, candor, helpfulness, and willingness to do what it took to secure me the best possible outcome was incredible.”

“We have used Sherman Bridge several times for our fix and flip needs. They are right there and totally on it when I call in a crunch needing money fast! We will stay with Sherman Bridge because of their prompt and get it done service.”

“We contacted Sherman bridge with a very short timeframe to be able to close and they helped us zip through the process with ease, helping us figure out how to overcome obstacles throughout the way to assure we’d get the best deal possible without wasting time nor resources.”

Previous

Next

Thank you for reaching out! One of our loan consultants will be in touch shortly.